Snipp Interactive Inc (TSX-V: SPN; OTC: SNIPF)

The purpose of this piece is to provide an overview over the company. It should serve as an introduction and place for reference for people new to the story.

First and foremost, we have three parts to the whole: The core business, Gambit and SnippMedia. More on these will be detailed later in the write up, but it is important to understand that SnippMedia has yet to contribute revenue (but is about to) and the core business is the cash cow that is generating the bulk of the revenues and profits with historical gross margins in the 50-70% range. In fact, the most recent drop in margins and profitability is entirely due to Gambit, which grew revenues explosively, and a temporary but heavy reinvestment period. Going forward and from now on, as I will elaborate, this will change, significantly and to the better.

Snipp is at a cross road in its evolution and with our understanding of the business, what has been, what is and what will be, we are significantly ahead of the curve. The opportunity for investors at this point in time could hardly be better.

Core Business

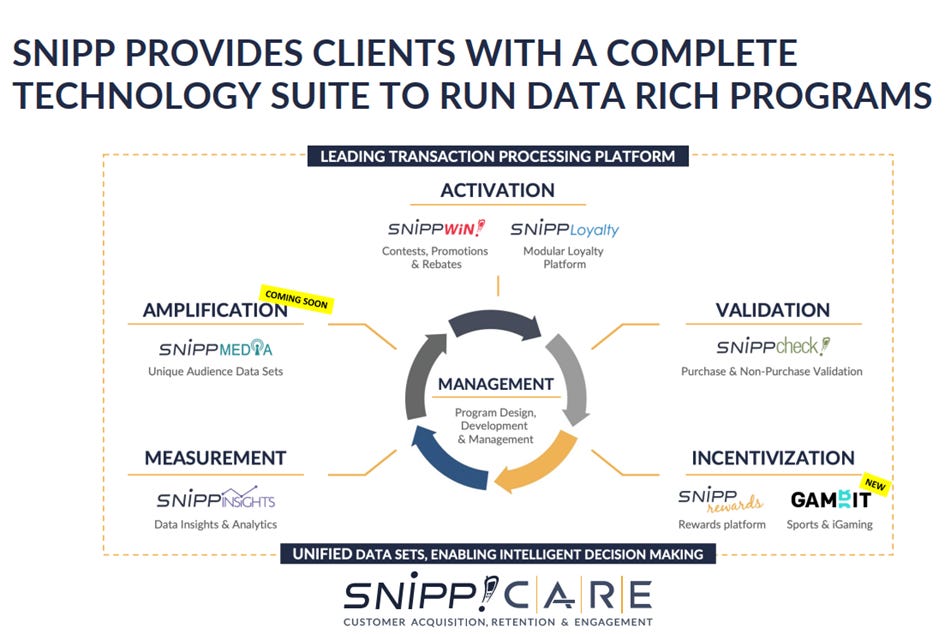

Snipp deems itself a platform as a service company. Call it PAAS if you’d like but you are likely the only one. The overarching theme of the company is to have “A single source of customer truth that is constantly evolving with richer and deeper data on customer habits, behavior and attitudes.” The platform offers access to 1st party data. That is the type of data that a consumer or customer gives to you directly, eg what products you bought yesterday at the grocery shop, where you live, etc. This is becoming more and more important to advertisers for targeting and on the backdrop of increasing privacy regulations. Snipp is getting access to these data sets from receipts that consumers scan and send. Why would they do that? Because they get rewards/loyalty points that way! The SnippCheck mobile receipt processing solution allows brands to execute customized purchase-based promotions and loyalty programs. It supports any qualification criteria and works across all retailers and all devices. SnippCheck is the industry’s leading receipt processing solution, currently supporting two of the largest CPG loyalty programs and having processed millions of receipts for hundreds of promotions. The company also has made available API Licensing for clients to incorporate into their own Apps and/or web ecosystems. Snipp performs loyalty and reward campaigns, promotions and the associated analytics. The company can offer a brand or CPG an unparalleled level of understanding of their customers, for example X% of people who buy Mars bars also buy Pepsi Cola and Y% buy Coca Cola. You get the idea.

Snipp generates revenues from this core business in various ways: licensing, services, platform customization (high margin) and redemptions (low margin) etc. There is some degree of lumpiness with campaigns, new contracts and so on, but about 50% of revenues are recurring like the text book would describe it, and even a large fraction of the rest is repeated business.

Snipp basically provides an end to end solution for their clients with very broad horizontal and vertical integration, but is in this core business dependent on the brands spending money for campaigns and has no control over the consumer audience.

Which brings us to the other two lines of business: the recent acquisition Gambit and built from scratch SnippMedia.

Gambit

With Gambit the company generates spendable budget “out of thin air” by capturing loyalty liabilities. It achieves this by allowing companies to rid themselves of these liabilities and the consumers to actually spend those points. Such a liability is - to give an example everybody knows - the collection of airline miles that airline customers have accumulated for which an airline has to deliver service in the future net of breakage. The size of these liabilities or customer assets is of the order of $100B and a Dave and Busters or Bally’s for example would obviously love to get rid of these…. And pay for it but also even benefit further with additional customer engagement. What Gambit does is convert these “points” into virtual currency with which people can play games and obviously win something. Importantly, you cannot put real cash to play, which means less regulation since it is officially not gambling. Nothing like this exists to date.

SnippMedia

With SnippMedia the company is able to control the audience. What I mean by that is in the core business Snipp cannot offer a CPG this and that many eyeballs. It is simply the number of people that actually buy the product and scan the receipt. But with SnippMedia, the company can approach a client and directly give them access to millions of people: We are talking about credit card holders. Several banks are in the pipeline but agreements exist already with Bank of America (launch in March after very successful trials) and Triple, a PNC subsidiary. That is an audience of roughly 47M for BofA for example. A lot.

The way it works is that Snipp utilizes the existing platform to offer rewards, deals, promotions etc within the credit card/banking app. In the BofA example, the bank simply grants Snipp access to the audience, Snipp does everything else. In a sense the company acts as a clearing house between, bank (consumer), retailers and brands. You activate your coupon swipe your card and boom % off for your purchase at … Walmart. Or you get a Pepsi for free. Etc. And this is unique about Snipp. They are the only ones to offer SKU level depth (in contrast to say Cardlytics). Of course, it also helps that Snipp has relationships to CPGs and retailers! It is further important to note that there is no cannibalization risk to the core business. These are separate budgets.

Keep in mind the motivations behind the actors. The retailers attract additional customers/purchases. “Oh I get % at my next purchase at Costco… that is where I go instead of Walmart.”. Or you may just do that additional trip to the store you wouldn’t do otherwise. The brands and CPGs gain tremendous customer insight and can target very specifically. The benefit to consumers should be obvious. Even the banks don’t otherwise know what you bought. They might know that you bought stuff for $52.37 at Costco (not useful for say Pepsi). They do not know that you bought product X and Y and Z etc. So they cannot really sell that data to brands for example without Snipp. It really needs that trifecta of bank/customer audience, retailers and brands/CPGs. And Snipp is in the middle taking a cut.

Economics and financials

Now that we know what Snipp does, let’s talk about the economics. The core business is with some fluctuations a 60-70% gross margin business. SnippMedia should do 50%. Gambit will in the immediate future become 30-50%. Until recently this was in the low single digit range because of the deal structure with the first customer swagbucks. This is ending. It was used to do product development, establish the business model etc. Going forward, swagbuck will be gone or get a new deal, much more favorable to Snipp. Negotiations are happening right now. The other client is Dave&Busters and there we are talking about 50%ish albeit at a lower revenue base.

Gambit is also the reason why the company began losing money recently and had terrible overall gross margins after years of profitability (3 years of profitable growth, 40%+ revenue CAGR). Let me say it again, this is ending. Going forward Snipp will again be a 55-65% gross margin business with growing profitability.

Q4 is not yet announced but we can expect more than $30M in revenue for the full year. Q1 should see a sequential revenue decline due to the aforementioned swagbucks deal ending, but gross margins will jump higher. I strongly expect overall growth for 2024.

The CEO has the aspiration to achieve $75M in revenue by 2025 through a mix of organic and inorganic growth.

Management

And let me tell you Atul is a master in structuring transactions and getting a brilliant deal for him and his shareholders in terms of ROI. He is founder of the business and one of the best CEOs I know. He is a very prudent capital allocator, extremely hungry for success and motivated, a savvy operator, frugal but also open to feedback from shareholders, available for questions, and a really nice and funny guy. But I would also highlight Tom Burgess, who runs SnippMedia as a brilliant addition to the team and also Christopher Cubba new Chief Revenue Officer and basically head of the core business. In general, the management team is very strong (even though Atul is going to hire a full time, Nasdaq level CFO) and has been significantly upgraded since the time that I first heard about the company. In fact, I am amazed by all the talent accumulated in this tiny company!

Minority Investment

Another highlight is that Bally’s bought a minority stake of 10% in 2022 at what was then a 40% premium for $5M (something like 20ct USD a share). A veteran microcap investor once told me that whenever he had a situation where a large company buys a stake in a small company at a healthy premium, it has worked out extremely well for the small company.

Valuation and Cap Structure

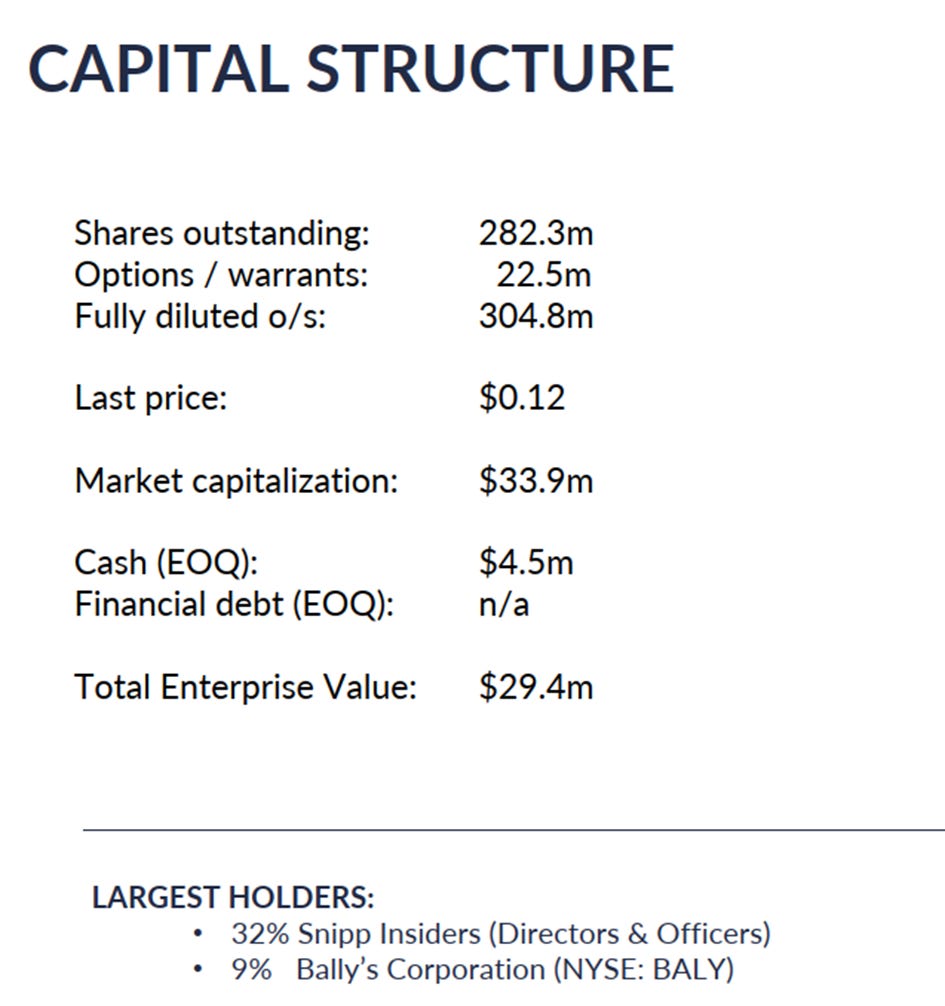

The balance sheet is pristine with no debt, $4-5M in cash and hardly any warrants or options, mostly in the hands of mgmt. for compensation. The float is also very tight. Beyond the insider ownership and Bally’s there are also a number of large holders so that the actual trading float is likely in the range 20-30% of all shares.

In terms of valuation, currently the EV is about USD 20M (below image is in CAD) and even if you assume only $50M in revenue instead of the aspired $75M at 10% EBITDA margins we are talking about a multiple of 4 in 2025. That’s for a rapidly growing business. If you assume little growth you also have to pencil in higher EBITDA margins of at least 20%. You do the math. Insanely cheap. I like to say you really only need one of the three lines of business to work out for SNIPF to be a solid investment.

The growth drivers will be the core business modestly, Gambit, and SnippMedia, which could really take off. Again, the launch with BofA is imminent, Triple to follow, and if these programs are successful, other banks will follow suit. Recall, the bank has 0 effort, it just provides the audience and takes a nice cut.

These are all massive markets and all these lines of business are extremely scalable for Snipp due to the software type nature and high degree of automation.

There will also be acquisitions, most likely of the small tuck-in nature. Atul is picky and has plenty opportunities on his table.

A final point relates to the exchange. The company is actively exploring ways to get on the Nasdaq. This could be the normal IPO type way, a merger with an NOL shell or a SPAC. I would assume this could happen within a year. It is a trade-off, because while the company could do such a deal right now, Atul wants the company to be in a perfect position to do so and achieve a more reasonable valuation.

Summary

In summary, you have a company

with strong leadership having lots of skin in the game

that is in an industry with massive addressable markets in all three lines of business

with strong tailwinds eg privacy regulations

that is imminently flipping from decreasing margins and losing money to increasing margins and growing profitability with strong revenue growth

that is extremely cheap on normalized forward looking numbers

with a fortress balance sheet and capital structure

of considerable experience and a proven business model

with a business model that is highly scalable and generates strong margins

that has many unique capabilities and competitive advantages

strong relationships to CPGs, brands and retailers

unique SKU level data (nobody else can offer this today)

an end to end solution for clients

1st party data at scale and associated analytics

A powerful and established tech platform

Gambit is absolutely unique and first in its capability to allow companies to eliminate their loyalty liabilities and for Snipp to monetize them

SNIPF is my second largest position and I am in for the long run.

Author’s Disclosure: We have a beneficial long position in the shares of SNIPF either through stock ownership, options, or other derivatives, no position in any other company mentioned. I wrote this post myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. I am not a licensed securities dealer, broker or US investment adviser or investment bank.

Breakout Investors’ Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Breakout Investors as a whole. Breakout Investors is not a licensed securities dealer, broker or US investment adviser or investment bank.