New but slightly speculative pick

...which really isn't that speculative any more

The below was published unedited for premium subscribers on April 3. Some updates follow at the end of the post. There is still a lot more to be said though and we have discussed ITMSF in detail multiple times in our Weekly Elite Subscriber Calls. The replays are available and I would encourage anybody wanting to get into the weeds to become a subscriber. You won’t be disappointed :)

As I touched on during yesterday's Elite call I have a new pick, which remains a little bit speculative but extremely promising. I am talking about Intermap Technologies.

About Intermap Technologies Founded in 1997 and headquartered in Denver, Colorado, Intermap (TSX: IMP; OTCQB: ITMSF) is a global leader in geospatial intelligence solutions, focusing on the creation and analysis of 3D terrain data to produce high-resolution thematic models. Through scientific analysis of geospatial information and patented sensors and processing technology, the Company provisions diverse, complementary, multi-source datasets to enable customers to seamlessly integrate geospatial intelligence into their workflows. Intermap’s 3D elevation data and software analytic capabilities enable global geospatial analysis through artificial intelligence and machine learning, providing customers with critical information to understand their terrain environment. By leveraging its proprietary archive of the world’s largest collection of multi-sensor global elevation data, the Company’s collection and processing capabilities provide multi-source 3D datasets and analytics at mission speed, enabling governments and companies to build and integrate geospatial foundation data with actionable insights. Applications for Intermap’s products and solutions include defense, aviation and UAV flight planning, flood and wildfire insurance, disaster mitigation, base mapping, environmental and renewable energy planning, telecommunications, engineering, critical infrastructure monitoring, hydrology, land management, oil and gas and transportation.

This is not an in depth write up. More research needs to be done but I would like to illustrate the opportunity.

The company has recently announced a large contract in Indonesia with a follow up of first cash having been received.

won a $20 million contract to map the Island of Sulawesi, Indonesia in 2024 (the “Contract”). The Contract is the first phase of the Indonesian national topographic basemap program to create a national digital basemap as part of the One Map program backed by Presidential Decree. Under the One Map program’s approved technical specifications, the government will collect airborne IFSAR-derived elevation data and cloud-free radar imagery for the entire country at resolutions suitable for 1:5,000 scale mapping. The first phase awarded today represents 10% of the country’s land area and 10% of the One Map program. Work on the remaining 90% is expected over the subsequent four years.

Even better, just minutes ago the company reported 2023 Results and 2024 Guidance

Subsequent to year end, Intermap announced the award of a material contract from the Indonesian government. This initial award includes an opportunity to repeat, with follow-on requirements to complete mapping the country during an additional 4-year period. Work on this contract commenced in February 2024. Including Indonesia, for the current year ending December 31, 2024, the Company projects total bookings in the range of $20-25 million, with $16-18 million in revenue and an adjusted EBITDA margin of approximately 25%.

So that is at least $4M adjusted EBITDA on a $30M market cap with ca 9 times that coming in the following 4 years.

So on the face of it I'd say the stock should be 2-3X higher, likely even more. IF THIS IS REAL.

Why would it not be real? The company had something similar in the DRC, which was much bigger and fell flat though likely not through their own fault except of relying too much on partners. A lot of investors got burned. There are more yellow flags. Management is almost impossible to reach, there is no cash received yet shown in an up to date balance sheet, it is hard to find verification from Indonesian sources.

However! They had a presence in Indonesia for a very long time and the deal is large but reasonable. Certainly not "too good to be true". There is new and highly reputable management and a very impressive board. There was even an insider buy right after the first announcement and the dilution in past years was kept to a minimum despite losses. There is an official Worldbank site for this mapping initiative (though without mentioning Intermap). The site Intermap set up to explain everything including case study looks really good.

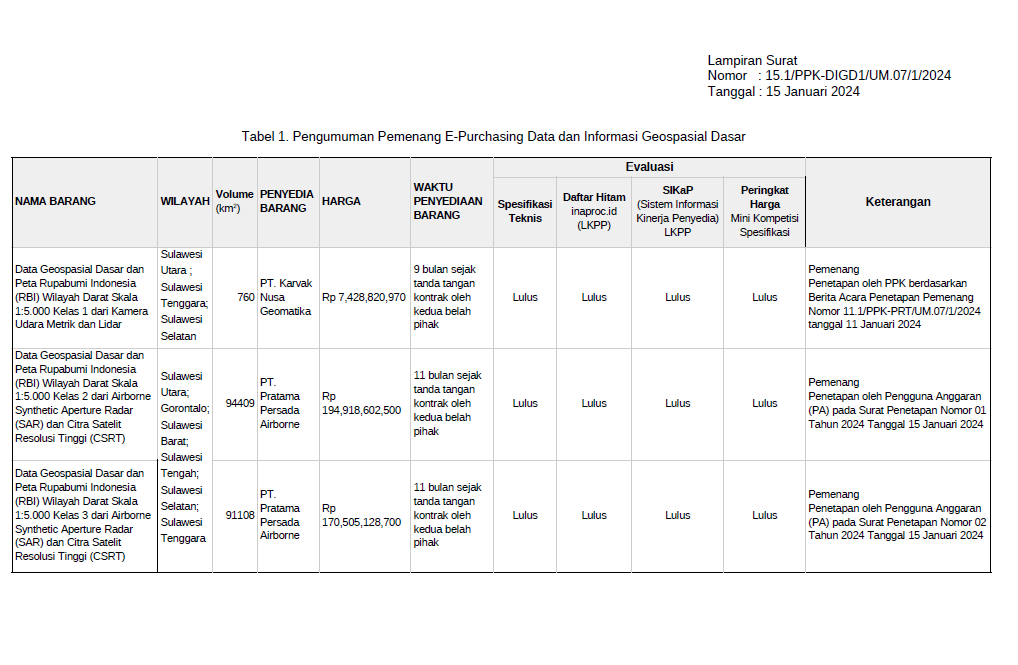

All of this is interesting and promising but not enough. After all, nowhere is Intermap named and information about their JV partner state-owned enterprise, PT Pratama Persada Airborne (PPA) is limited.

But here is what convinced me. I was able to identify the official award of Indonesia’s national geospatial agency, Badan Informasi Geospasial (BIG) to PT Pratama Persada Airborne. Granted, Intermap is still not named, but all the other details match exactly, like Sulawesi, the square miles, and even the timing (it came out days before Intermap's first announcement). So, this is not 100% proof but as good as it gets with some uncertainty left.

So this is our opportunity: The above document is really hard to find and in Indonesian language. I may well be the only one to have found and understood it in the context of Intermap. A lot of investors are rightly skeptical having been burned in the past and it is a Canadian microcap, so not many are even paying attention. The stock has reacted but by far not enough....but now with guidance out maybe that changes. It should!

Putting it all together, this is enough for me to have a solid position.

UPDATE July 23:

My conviction is now substantially higher and this is becoming a top pick for me.

I was on Mark Gomes’ show to discuss Intermap: LINK

Mark indirectly participated in the recent financing

The company is closing a financing, which they had tremendous demand for. Unfortunately, the company was too upfront about it and caused the recent weakness amongst other things. But this seems to be the clearing event.

The offering document calls for NTM revenue of ALREADY contracted $25M. So there is room to the upside and it barely trades over 1 times NTM sales. That is about 4 times EBITDA.

The CEO owns a huge piece of the company now after continuously putting his own money in (I believe maybe even close to 50% or so).

We will know in August/September if the World Bank funds the other 90% of the project. However, I have found documentation and a quote from a World Bank official indicating this to be more of a formality.

We had the opportunity to speak to the CEO and were very impressed. He has really cleaned up and set the co up for success. Even if the Indonesian win isn’t coming through fully, the rest of the business is doing extremely well also.

If the funding comes through though, they are pretty much set in stone having spent years being certified and literally helping write the specs.

If they do win the other 90% the EBITDA margins will be substantially higher than 25%.

There is your recipe for a huge winner: Lots of skepticism and burned investors, informational advantage for us, high insider ownership and motivated mgmt, very large revenue growth opportunity with increasing margins and a cheap valuation.

Author’s Disclosure: I have a beneficial long position in the shares of ITMSF either through stock ownership, options, or other derivatives. I wrote this post myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. I am not a licensed securities dealer, broker or US investment adviser or investment bank.

Breakout Investors’ Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Breakout Investors as a whole. Breakout Investors is not a licensed securities dealer, broker or US investment adviser or investment bank.

Excellent research Florian!

Was great listening to you in Money Mark. Was able to snag a small position of 8,000 shares at $0.40.