Is Intermap Technologies the lowest-risk, highest-reward investment I own?

$IMP.TO, $ITMSF

What multiple would you give a company growing revenues at 158%, already profitable, debt-free, and with a mega-project 7x the size of its entire 2024 revenue (50% cash flow margins) almost in the bag? How about less than 2x sales or less than 5x the NTM EBITDA?

Introduction

When I add companies to my investment tracker, I usually initiate them on Substack to have a reference point I can refer back to. It’s my way of keeping accountability and trackability to my investment picks. Usually, that comes in a longer research report, but being as stretched for time as I am (I’m moving to the US in 4 days), a short writeup outlining the thesis will have to suffice.

Last week, I added three names to my model portfolio. I forgot to add Intermap Technologies ($IMP.TO or $IMTSF). I’ve been invested in Intermap since July 17th, and my cost basis is CAD $0.60. The stock is now up to CAD $0.90, which is 50% up. There’s still plenty of upside, and the downside has reduced since I bought in. I have yet to sell any shares despite being potentially overbought technically.

Credit to

for finding this company and doing a lot of the heavy lifting on the research for this pick.Company background

Note: this introduction was generated by AI and edited by me (to save time).

Intermap is a company that specializes in creating high-resolution 3D models of the Earth's surface. It uses various technologies, such as aerial and satellite imagery, LiDAR (Light Detection and Ranging), and other geospatial data, to create these models.

Here are some of the key things Intermap does:

Data Acquisition: They collect data from various sources to create their 3D models.

Data Processing: They process and analyse the collected data to create accurate and detailed models.

Data Delivery: They deliver their 3D models in various formats and through different platforms, including web services and software.

Their services are used in a wide range of applications, including:

Urban planning and development: Creating detailed 3D models of cities to help with planning and infrastructure development.

Natural resource management: Mapping and monitoring forests, mining areas, and other natural resources.

Disaster response: Providing accurate 3D models of disaster-affected areas to aid in rescue and recovery efforts.

Defence and security: Creating high-resolution models for military operations and intelligence gathering.

Telecommunications: Planning and deploying telecommunication infrastructure.

Insurance (e.g. against natural disasters): To help correctly price premiums.

Overall, Intermap plays a significant role in providing accurate and detailed 3D models of the Earth's surface, which are used in various industries and applications.

Momentum

Management recently reaffirmed guidance of $16-18m in revenue this year. For reference, they had $6.2m in 2023. Yes, that is a 158% revenue growth rate. Q2 revenue came in at $3.6m, more than double the $1.7m in Q1.

Operating margins came in at 17.6%, compared to a negative in Q1.

25% EBITDA margins are forecasted for the year. If they are awarded the rest of the Indonesia project (very likely), this could reach 50%.

The expanding pipeline is now worth $380m. Governments in Indonesia, Malaysia, Malawi, India, and Greece have awarded notable contracts.

Just yesterday, Intermap was awarded the second phase of its prime contract with the U.S. Air Force to support its development of navigation solutions for GPS-denied environments. The expansion of this contract certainly increases my conviction of Intermap’s value proposition and technology, de-risking the investment above the financial reward the expansion will bring.

In terms of price momentum, the stock has traded in a well-defined range since 2022, and it’s been consolidating since 2020. That said, you can see it hitting up against the top of this range currently.

You can see this range continuing to play out in the 1-year chart. The momentum is clearly up for the time being. The stock had a huge jump in July, up around 50%; it retraced almost half of that move, then headed back up and recently shot past the July high and was up 17% yesterday, briefly hitting the upper level of the range at $0.95. If/once the stock breaks this level of $0.95, there’s a lot of room to run without notable resistance levels.

Monopoly

I’ll quote the CEO as he explained it well in a recent presentation:

What we do is so unique that we don't see exact competitors. Take Indonesia. They have an open electronic procurement bulletin board; you can see all the bids, including the prices and who applied. Most of them are local.

I should emphasize that Intermap's key capability is that we operate on a country and global scale. Smaller companies do ground surveys or use low-altitude aeroplanes, drones, or easier sensors like optical or lidar. They'll show up and compete for certain things, but they'll never beat us in our market, which is a large scale. Nobody can beat us in Indonesia because we're doing the whole country. They can't compete with that, so you'll see subsets of what I call sub-competitors, both on the application side (in terms of rendering) and the data collection side. You'll see all kinds of players, a whole variety. Still, in terms of a global scale, a 3D living, breathing elevation model available on demand within a fraction of a second - points anywhere - I really can't think of anybody who can do that perfectly.

Essentially, they’re the only company that can do both scale and precision simultaneously. It’s a difficult market to enter, as much of the data collection requires permissions from governments, militaries, and so on. It’s also technologically difficult to compete and would require large amounts of time and capital to catch up. A final barrier to entry would be that the contracts are built upon relationships which Intermap has been building for years.

Management

The CEO has been in the industry for around 15 years and has plenty of experience. Based on interviews, I like him, and he seems to have a sensible approach. I liked this quote from him for a recent presentation.

We have a highly educated, mostly long-tenured employee base. The motivation in the employee base is around not just solving problems but also having a long-term perspective on how we solve those problems. We run lean in that our really smart people are working hard on stuff they're very engaged in. It doesn't mean many mediocre people are counting pennies and working 9 to 430. Our people are working 24/7, around the clock. They're stretched, but there's a lot of operating leverage in the business model.

This ticks a lot of boxes for me: long-term-focused management hiring similarly focused employees. Also, they prioritise quality over quantity in terms of team members. If the employees are long-tenured, I assume they are enjoying the job, though this may be worth checking since he said they are stretched.

The CEO is heavily invested in the company, owning 15% of the shares, mostly bought with his own cash. There’s been no insider selling of late.

They have very low stock-based comp, which has stayed at around $100k a quarter for years.

Margin of safety

The downside seems tiny at this point. The company has minimal debt and just finished a round of funding, so it has sufficient capital to set up the upcoming projects.

The company is profitable and growing nicely. It’s trading at around 1.6x 2024’s forecasted revenues. A recent offering document put NTM revenues at $25m, which would put the price-to-sales ratio at 1.1x. EV is less than 7x this year’s forecasted EBITDA or 5x NTM forecasted EBITDA.

If the business continues to grow and expand, which is highly likely given the contracts they have in hand, it’s hard to imagine investors going wrong at these valuations.

Multi-bagger upside

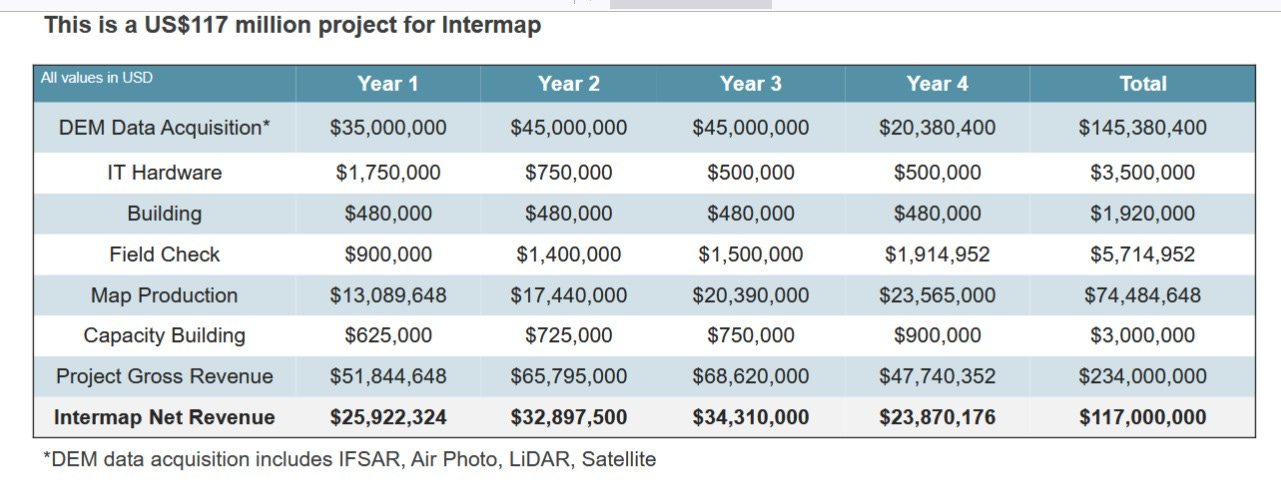

The Indonesia island mapping project alone has tremendous upside. They have currently been awarded about 10% of the total project and have been paid a portion of that amount already. The other 90% of the project is technically yet to be awarded (likely in Q1 2025), however, there is realistically no way any other company will be awarded the contract. Intermap has unmatched capabilities, has a foot in the door, and is the partner of choice. The question is whether the rest of the project will be funded by the World Bank. The funding decision will be made by September 23, 2024. People close to the company believe it is very likely this will be approved.

This project is worth around $120M over 4 years and could reach EBITDA margins of 50%. For reference, that project alone would generate around $40m in revenue annually, which could produce around $20m EBITDA. Putting an 8x multiple on this project alone could justify a share price of $160m. That’s in addition to the rest of the business, which is doing well.

I will note that while the data collection part of the contract (covered above) is a one-and-done deal, the project would begin to generate perpetual maintenance revenue from software and data services going forward.

The market price would indicate that the market does not believe this project will materialise. If it does, it’s hard to see the stock price not at least triple once the 90% is awarded and then once the cash inflows continue to ramp up. The official award is in Q1 2025, and remember, they are already getting revenues, so the timeframe is tight. If it doesn’t, well, that’s covered by the progress of the rest of the business (covered under the margin of safety).

Summary

Yes, this is probably now my lowest-risk, highest-reward investment. If Indonesia works out, this will be a home-run investment within a year (at least a triple). If Indonesia is delayed or the funding doesn’t come through (unlikely but possible), I don’t believe the stock will struggle too much, as I don’t think the stock is pricing it in anyway.

Well if buyers wanted in then I think today is a good day as it is down almost 10%. I added a bit at about -5%. So will try and top that off and get to 25,000 shares

I would say being a one and done and given the rapid increase in price the current contract (10% portion) is priced in the stock price. The remaining is not.

There is history of contract not materializing and that could be why the remaining piece is not priced in. So it does provide opportunity if conviction is high that the other 90% will be funded and they get the contract. The funding is key to me as I do believe they will receive the contract if/when funding is approved.

I don’t own much and own it on the US exchange. Only 11,500 shares. Up 56% currently.