Intellinetics: Scalability Engine Set to Roar

Intellinetics: Scalability Engine Set to Roar

A guest article by Sergio Heiber

NOTE: The article below was submitted by Sergio Heiber, a fellow Seeking Alpha author and microcap investor. We hope our followers appreciate his contribution. Sergio hopes to continue coverage of this name through Breakout Investors’ platforms.

Intellinetics (INLX) is a small company competing for market share in the massive market opportunity in the fragmented cloud-based document management industry. Management has targeted attracting customers in niches such as school districts, government agencies and non-profit agencies, where the revenue opportunity from each respective customer is too small to capture the interest of the larger competitors.

Intellinetics is profitable, has an improving balance sheet and sells at a discount to its peer group. The company is recognized as one of America's fastest growing companies and reported strong results for fiscal 2023 despite a weaker fourth quarter than in fiscal 2022. The stock price declined by about 30% after the 2023 financial report, probably in line with the general market sell-off or profit taking as the stock price had been on a steep runup.

My investment thesis is that a newly introduced automated payment processing system will accelerate revenue growth and profitability by attracting new customers and offering cross-selling opportunities with existing customers.

Building the Scalability Engine

Intellinetics' document processing platform, IntelliCloud, was developed in collaboration with Intel (INTC) and commercially introduced in 2015, serving mostly government agencies. IntelliCloud is a document conversion and document management platform for converting documents into digital form and storage in the cloud. Customers sign a software as a service ("SaaS") recurring revenue contract to access, manage and analyze the data.

The acquisition of Graphic Sciences in 2020 added scanning and microfilm services to the IntelliCloud platform and brought along what has been and continues to be the company's two largest customers The State of Michigan and Rocket Mortgage (RKT). Intellinetics expanded its digital services to K-12 school districts by acquiring Yellow Folder and CEO Imaging Systems in 2022. Intellinetics currently serves about 600 K-12 school districts, with each respective district adding annual revenue of about $8000, on average.

Intellinetics has developed the IntelliCloud Payables Automation System ("IPAS") as a solution for Intellinetics customer On Top of the World, a Florida based home builder. On Top of the World is also a Constellation HomeBuilder customer which led to a Intellinetics collaboration with Constellation.

IPAS is integrated with Constellation's Newstar ERP software and applies machine learning and artificial intelligence technologies to the entire range of billing and payment processing functions such as coding, managing workflows, certifications, billing and analytics. The partnership places Intellinetics inside the ecosystem created by Constellation, bridging builders and homebuyers. Nine home builders have signed on as IPAS customers which is expected to add $500K in 2024 revenue. That translates to an average of $55K per customer in annual recurring revenue.

Scaling Opportunities

Intellinetics continues to add to its government and school district customer base such as a recently announced contract with two departments of a Michigan municipality and a ransomware protection contract with a Mississippi school district. The need for cybersecurity will provide a tailwind for Intellinetics gaining new contracts from school districts and government agencies.

Management expects to sign on additional home builder customers this year. President and CEO Jim DeSocio said at the 2023 earnings call last week, "We expect to more than double the customer count in this business over the next few quarters."

The company is also seeking to cross-sell a stand-alone version of IPAS to its existing customers and is currently in beta testing mode with one K-12 school district. There is also an intention to expand into other industries in partnership with Constellation and through additional partnerships.

Partnerships

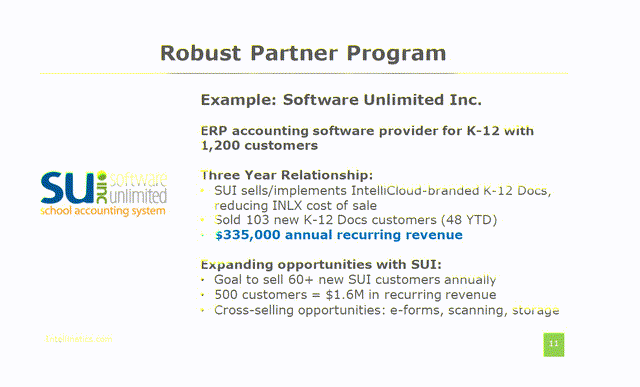

The company lists several partners on its website beyond the recent Constellation collaboration. Two key partners are Applied Innovations, formerly known as Applied Imaging and Software Unlimited. The former includes the Intellinetics platform in the digitalization of its copier customers and the latter has been instrumental for Intellinetics introduction into new K-12 school districts.

Competitive Landscape and Valuation

Cloud-based document management was accelerated by Covid across all industries creating a massive $50 billion industry. In seeking to attract small to medium size enterprises, Intellinetics competes in a fragmented sector populated by private companies such as DocuWare, Square 9, M-files, On-Base, FileBound, Frontline, Laserfiche, and Harvest Technology Group. Power School (PWSC) is the market leader in the K-12 school district cloud services market.

Up till now Intellinetics has been able to work in conjunction with PowerSchool in about 50 school districts with the former providing student record services and the latter providing school financial activities services. The introduction of IPAS allows Intellinetics to offer cloud based automated financial functions to school districts.

I selected Iron Mountain (IRM), a publicly traded industry leader in document management and storage and PowerSchool for comparison with Intellinetics. Intellinetics is a tiny company with a market cap of $30 million while IRM and PWSC have market caps in the billions and may not be valid comparisons, nevertheless, INLX is growing faster and selling at cheaper multiples than its giant competitors, making it an attractive acquisition target.

INLX IRM PWSC

P/S 1.73 4.00 4.08

EV/S 2.01 6.71 5.93

EV/EBITDA 12.00 20.07 31.89

P/B 3.03 103.66 2.21

Y/Y REV GROWTH 20.47 7.38 10.62

Financial

INLX uplisited to the NYSE American in Sept. 2022. There are about 4.7 million shares outstanding, fully diluted. Insiders own about 45% of the shares. Three insiders increased their positions earlier this month.

The market cap is almost $30 million. Reported cash is $1.2 million and $3 million in debt as of the end of 2023. The EV is about $32 million. Management has announced that debt will be reduced by $500K this year and expects to be net cash positive by the end of 2024. The reported net account receivables of $1.8 million along with the cash position is sufficient to fund operations for 2024 and beyond as the company increases its profitability.

Total revenue for 2023 was almost $16.9M, 22% higher than the prior year as the company increased its recurring revenue. This figure includes only two IPAS customers that were uploaded to the cloud late in the year. Intellinetics has reported gross margins of about 63% over the last two fiscal years. Increasing revenue from IPAS and providing software services such as cybersecurity, SaaS recurring revenue, will increase the company's overall gross margins. On average, SaaS recurring revenue results in 73% gross margins.

For the Years Ended December 31,

2023 2022

Revenues:

Sale of Software $100,260 $ 159,084

Software as a Service 5,133,215 4,017,409

Software Maintenance Services 1,407,064 1,387,885

Professional Services 9,167,428 7,357,937

Storage and Retrieval Services 1,078,414 1,094,613

Total Revenues $16,886,381 $14,016,928

Data is from a press release.

Risks

The largest two customers, The State of Michigan and Rocket Mortgage, bring in almost half of the total company revenue. The over dependence on just two customers will decrease as the company expands its revenues, but it appears that there is little risk in losing these two key customers. Customers are sticky due to the inconvenience, interruption of services and cost in switching to a competitor. The State of Michigan contract is up for optional one year extension this September, and a full extension in 2025. Michigan has been a customer for 20 years and is further incentivized to remain a customer as it is a reseller that profits from contracting Intellinetics' services to state agencies. Rocket Mortgage is up for renewal at this time with terms being negotiated.

The company is dependent on hosting services from Amazon Web Services, Expedient and Corespace for its products as well as Microsoft technology.

The largest shareholders are Michael and Robert Taglich along with other Taglich Brother associates. The Taglich Brothers provide sponsored coverage on the stock and have provided financing to fund acquisitions. The Taglich Brothers have significant shareholder voting power which may not be aligned with other shareholders.

Spruce Point Capital Management put out a short thesis on PowerSchool last week. Much of the argument cited factors relative solely to PowerSchool but a slowing down of K-12 school district spending on technology is also mentioned. This report did not have any noticeable impact on PowerSchool's share price.

It does appear that K-12 school district conversion to the cloud is almost entirely completed but the districts will need to add services such as cybersecurity, which fits perfectly with INLX switching gears to focus on SaaS sales.

Conclusion

Intellinetics is profitable and fast growing. The balance sheet is improving with the reduction of debt. The company has established the framework to scale its cloud services business within the highly regulated K-12 school market and government agencies market. It has a potentially lucrative new market entry into the homebuilding industry with its automated cloud payment system. The company has created several opportunities to scale by cross selling the automated system and entering new market segments through existing and new partnerships. Margins and profitability will improve should the company continue to successfully shift its focus to SaaS recurring revenue.

Author’s Disclosure: I have a beneficial long position in the shares of INLX either through stock ownership, options, or other derivatives. I wrote this post myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. I am not a licensed securities dealer, broker or US investment adviser or investment bank.

Breakout Investors’ Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Breakout Investors as a whole. Breakout Investors is not a licensed securities dealer, broker or US investment adviser or investment bank.